Expert, Former Commissioner Testifies on Louisiana's Insurance Market.

Former Missouri State Insurance Commissioner Jay Angoff recently testified before the Louisiana Senate Judiciary A Committee. The former commissioner reviewed Louisiana’s insurance regulations, other states’ laws, and information provided by insurance companies to the National Association of Insurance Commissioners (NAIC). Mr. Angoff provided a detailed, data-filled report on Louisiana's insurance market. He explained how lax regulations that make Louisiana an extreme outlier contribute to high insurance rates. Additionally, he discussed the high returns insurers are seeing on policies in Louisiana and the massive profits rolling in on investments on their $1 trillion surplus.

Below are highlights from the hearing and a copy of Mr. Angoff's complete report and testimony.

Crisis for you, not them:

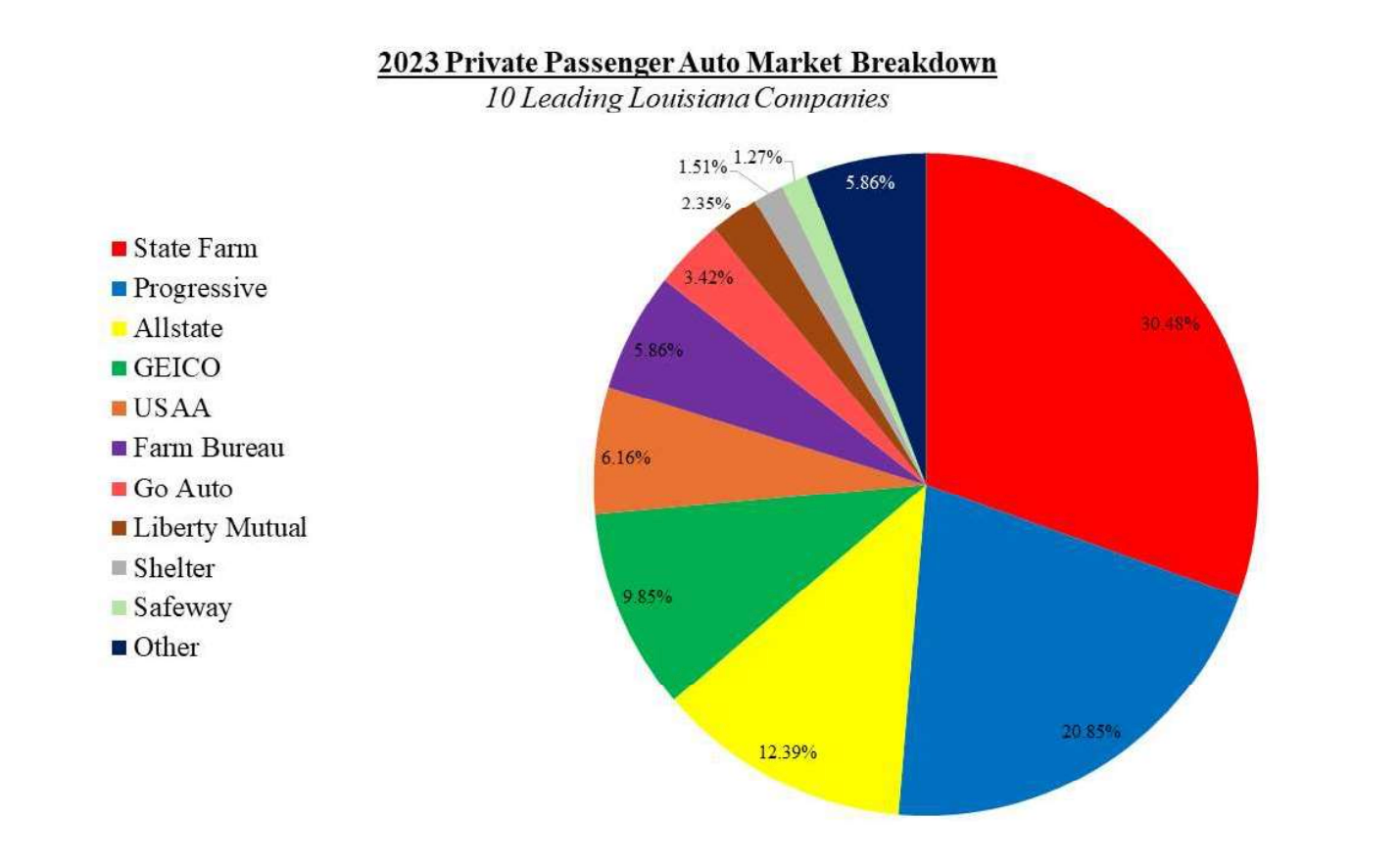

Commissioner Tim Temple and insurance lobbyists claim that insurers are struggling in Louisiana. But data from the National Association of Insurance Commissioners suggest otherwise. Jay Agnoff explains that, while severe weather poses a major challenge, insurers are thriving on high rates and low loss ratios.

Litigation or Lax Regulation?

Angoff explains why high insurance rates in Louisiana are due to severe weather and industry-friendly lax regulations, not litigation in Louisiana. He cites a major actuarial study on Louisiana's insurance market conducted by major insurers to determine what impact legal reforms would have on rates. The study found that legal reforms would have virtually no impact on the cost of insurance for policyholders.

Expert Explains the Role Lax Regulation Plays in High Rates:

Jay Angoff explains that Louisiana law allows the commissioner to reject a rate for being too low, but does not grant the commissioner sole authority to reject a rate for being excessive. Mr. Angoff also explains that he found "really, really high" profit factors in rate filing he reviewed in Louisiana.

This is consistent with a Harvard School of Business report that found “higher [insurance] premiums are being charged in states where regulators apply less scrutiny to requests for rate increases.”

Insurance Business Revolves Around Investment Income, not Just Selling Policies:

Commissioner Temple, big insurance companies, and their lobbyists want policyholders to believe that the business of insurance revolves around selling policies. But that's only the beginning. Insurance companies are investment banks that write policies to finance their investments. Jay Angoff explains that insurers reported $88 Billion in investment income last year, a 126% increase and an 8.25% return on their $1 Trillion surplus!